Foreign Earned Income Exclusion Revisited: Eligibility, Waiver, and Planning Opportunities

Foreign Earned Income Exclusion: Time Travel

Modern day foreign earned income exclusion has its origin in 1926, when Congress enacted its predecessor as part of a strategy to help American businesses expand overseas by incentivizing Americans to work and live abroad.[1] The exclusion is still the best-known, although sometimes misunderstood, tax benefit available exclusively to U.S. expatriates.

Misconception about Tax Return Filing Requirement

One of the most common misconceptions about foreign earned income exclusion is that there is no need or urgency to file a U.S. tax return if the taxpayer's compensation can be fully excluded by the foreign earned income exclusion. This cannot be further from the truth. In fact, the exclusion is only allowable by elections that must be made either with the original or an amended federal income tax return for the first tax year the election is to be effective. An election once made remains in effect for that year and all subsequent years unless revoked.[2] Taxpayers who do not file a return or follow the prescribed regulatory procedures for late election could become ineligible for the election and liable for tax on compensation that could otherwise be excluded.[3]

The Good News and the Bad News

We always prefer to start with the good news: Qualified individuals may separately elect to exclude from gross income the following:

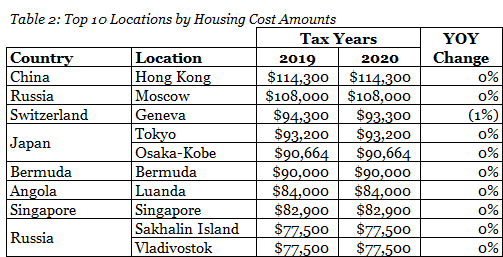

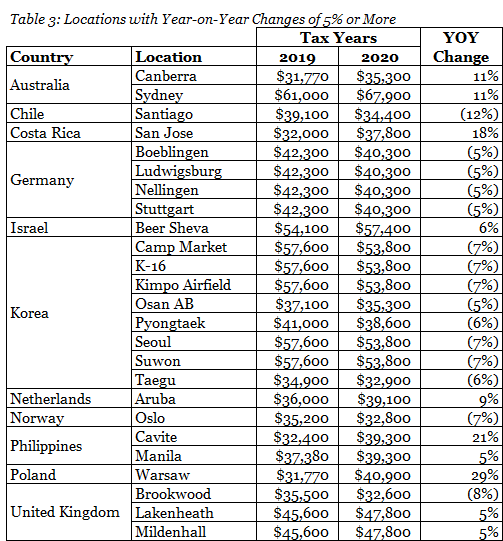

While the housing cost amount is standard for most locations, the statute authorizes the Treasury Secretary to adjust the limitation for specific locations based on geographic differences in housing costs relative to those in the United States.[4] The annual update for tax year 2020 was published by the Treasury Department and the Internal Revenue Service (IRS) in Notice 2020-13. In this year’s update, there are 33 entries with increases, 119 entries with no changes, and 99 entries with decreases. Hong Kong continues to retain its title as the location with the highest housing cost amount. See Tables 2 and 3 below for the limits applicable to selected locations.

This means expatriates can potentially exclude a substantial amount of their compensation from taxation. What is the bad news then, you might ask? The bad news came when the Tax Increase Prevention and Reconciliation Act of 2005 (TIPRA) was enacted.

One of the most significant impact of TIPRA was that, effective tax year 2006, any foreign earned income exclusion allowed on the return must be taken into account as if the taxpayer had not elected the exclusion in determining the rates at which any income should be subject to tax. Many expatriates still mistakenly believe that the taxable income as shown on the return is subject to tax at the lowest brackets.

In practice, this does not affect expatriates whose compensation and other income can be fully eradicated by the foreign earned income exclusion and standard deduction or itemized deductions. For others, the remaining income will be subject to tax at higher marginal tax rates. But this piece of news is not half as bad as it sounds when you compare the resulting tax burden against that of a domestic employee, all else being equal.

How to Qualify for Foreign Earned Income Exclusion

To be a “qualified individual” eligible for the foreign earned income exclusion, you must have a “tax home” in a foreign country and are:[5]

- A U.S. citizen who is a bona fide resident of a foreign country or countries for an uninterrupted period that includes an entire tax year (Bona Fide Residence Test)[6]; or

- A U.S. citizen or a U.S. resident alien who is physically present in a foreign country or countries for at least 330 full days during any period of 12 consecutive months (Physical Presence Test).

The term “tax home” has the same meaning as it relates to traveling expenses while away from home. You may have a foreign tax home if your work is in a foreign country and you expect to be employed in the foreign country for an indefinite, rather than temporary, period of time[7]:

- If you expect it to last for more than 1 year, it is indefinite;

- If you expect your employment away from home in a single location to last, and it does last, for 1 year or less, it is temporary unless facts and circumstances indicate otherwise;

- If you expect your employment to last for 1 year or less, but at some later date you expect it to last longer than 1 year, it is temporary (in the absence of facts and circumstances indicating otherwise) until your expectation changes.

You do not have a foreign tax home if your abode remains in the United States (where you keep closer familial, economic, and personal ties) unless you work in a Presidentially-declared combat zone in support of the Armed Forces of the United States.[8]

What If I Had to be Evacuated to the United States Unexpectedly Due to Adverse Conditions?

Congress recognizes taxpayers may be required to leave the foreign country before meeting the minimum time requirements (under Bona Fide Residence Test or Physical Presence Test) for foreign earned income exclusion due to war, civil unrest, or similar adverse conditions. The statute, therefore, provides that a taxpayer will be treated as a “qualified individual” if the following conditions are satisfied:[9]

- The taxpayer left the country during a period for which the Treasury Secretary, after consultation with the Secretary of State, determines that individuals were required to leave due to such conditions that precluded the normal conduct of business; and

- The taxpayer establishes to the satisfaction of the Treasury Secretary that he/she could, but for those conditions, reasonably have been expected to meet the eligibility requirements.

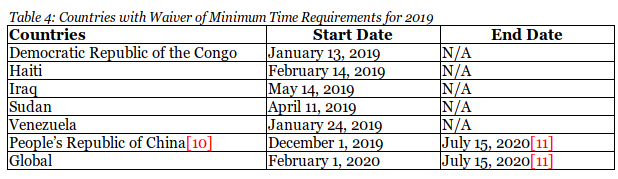

Historically, revenue procedures are issued by the IRS each year to list the countries to which the waiver of minimum time requirements because of war, civil unrest, or similar adverse conditions will apply.

For tax year 2019, the first list of countries, unrelated to COVID-19, was published in Rev. Proc. 2020-14 as part of the annual process. Rev. Proc. 2020-27 was subsequently issued as a result of evolving developments regarding the COVID-19 pandemic. See Table 4 for a summary of the countries and periods covered by these revenue procedures:

These waivers are country and date specific. Taxpayer relying on the waiver must have:

- established residency or been physically present in a specific country on or before the relevant start date; and

- departed on or after the start date.

For example, for the waiver in relation to China to apply, the taxpayer must have established residency or been physically present in China on or before December 1, 2019. Taxpayers whose residency or presence in China started on or after December 2, 2019 will not be eligible for the waiver.

Illustration 1

Facts:

- Reasonable Expectation: Mr. Wright’s 3-year assignment in China started on September 1, 2019 and was due to end on August 31, 2022

- September 1, 2019: Arrived in China

- January 10, 2020: Departed from China due to the COVID-19 emergency

Effect of Waiver: Mr. Wright would be a qualified individual for the period from September 1 through December 31, 2019, and for the period from January 1 through January 9, 2020, assuming he has met the other requirements to qualify for foreign earned income exclusion.

Illustration 2

Facts:

- Reasonable Expectation: Ms. Day has an open employment agreement to work in the United Kingdom for an indefinite period beginning January 1, 2020

- January 1, 2020: Arrived in the United Kingdom

- March 2, 2020: Departed from the United Kingdom due to COVID-19 emergency

- August 25, 2020: Returned to the United Kingdom for the remainder of the calendar year

Effect of Waiver: Ms. Day would be a qualified individual for 2020 with respect to the periods between January 1 through March 1, 2020, and August 25 through December 31, 2020, assuming she has met the other requirements to qualify for foreign earned income exclusion.

Options and Pitfalls

Most often, foreign earned income exclusion is utilized in conjunction with foreign tax credit albeit only for taxes paid or accrued on non-excluded income. There are, however, opportunities for tax optimization by electing the exclusions of foreign earned income and housing cost amount separately or not at all, in favor of foreign tax credit.

It should be noted that inclusion of income and credit for foreign taxes inconsistent with election(s) previously made for foreign earned income exclusion and/or foreign housing cost amount constitute revocation of the relevant election(s).[12] Such a revocation will render a taxpayer ineligible to make the same election(s) until the 6th year following the tax year for which the revocation was first effective.[13]

For example, if you had elected to exclude your foreign earned income and housing cost amount on a prior year return and decide to forego these exclusions on your 2019 return in order to claim foreign tax credit in full, you will be considered to have revoked those elections. As a result of the revocation, you will not be eligible to make another election for foreign earned income exclusion or housing cost amount until tax year 2025.

Treasury regulations, nevertheless, provide that a taxpayer wishing to re-elect the same exclusion before the 6th year after the revocation may apply for consent to do so by requesting a ruling from the Associate Chief Counsel of the IRS.[14] In deciding whether to give approval, the IRS will consider any facts and circumstances that may be relevant. Since requesting a ruling can be complex and the IRS will charge a fee for issuing these rulings, you may need professional help.

In conclusion, decisions to elect for or change the use of foreign earned income exclusion and foreign tax credit should be made only after careful planning and analysis.

[1] Postlewaite, Philip F., & Stern, Gregory E. (Oct 1979), Innocents Abroad? The 1978 Foreign Earned Income Act and the Case for its Repeal. Virginia Law Review, 65(6), 1093-1094.

[2] Treas. Reg. §1.911-7

[3] McDonald v. Commissioner, TC Memo 2015-169 and Redfield v. Commissioner, T.C. Memo. 2017-71

[4] IRC §911(c)(2)(B)

[5] IRC §911(d)(1)

[6] Also applicable to U.S. resident alien who is a citizen or national of a country with which the United States has an income tax treaty in effect. Green card holders, however, are advised to consult their immigration attorney prior to electing for foreign earned income exclusion on this basis.

[7] Rev. Rul. 93-86, 1993-2 C.B. 71 and IRC §162(a)(2)

[8] IRC §911(d)(3)

[9] IRC §911(d)(4)

[10] Excluding Hong Kong and Macau

[11] Unless extended

[12] Rev. Rul. 90-77

[13] Treas. Reg. §1.911-7(b)(1)

[14] Treas. Reg. §1.911-7(b)(2)

American Expatriate Tax is a part of Contexo Global Mobility Solutions & Tax Consulting Ltd. registered in Hong Kong. Together, we help companies and individuals navigate through the complexities of global mobility and related tax issues. Here is where you will find a blend of expertise from Big 4 accounting firms and Fortune Global 500 companies but the attention of a boutique consulting practice. The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.