GOP Tax Bills: Individual Provisions of Key Interest to U.S. Expatriates

With the House advancing the amended Tax Cuts and Jobs Act for a vote, the Senate has also released its own version of the tax bill (technically only a “Description of the Chairman’s Mark“), which is scheduled for markup, starting November 13, 2017. While similar, there are a number of differences between the Senate and House tax bills; to help you make sense of the provisions that could impact expatriates, we have outlined the key differences as well as commonalities in this newsletter. As mentioned in our previous newsletter, it is expected that further changes will be made along the way before this becomes law, if approved by the Congress and signed by the President.

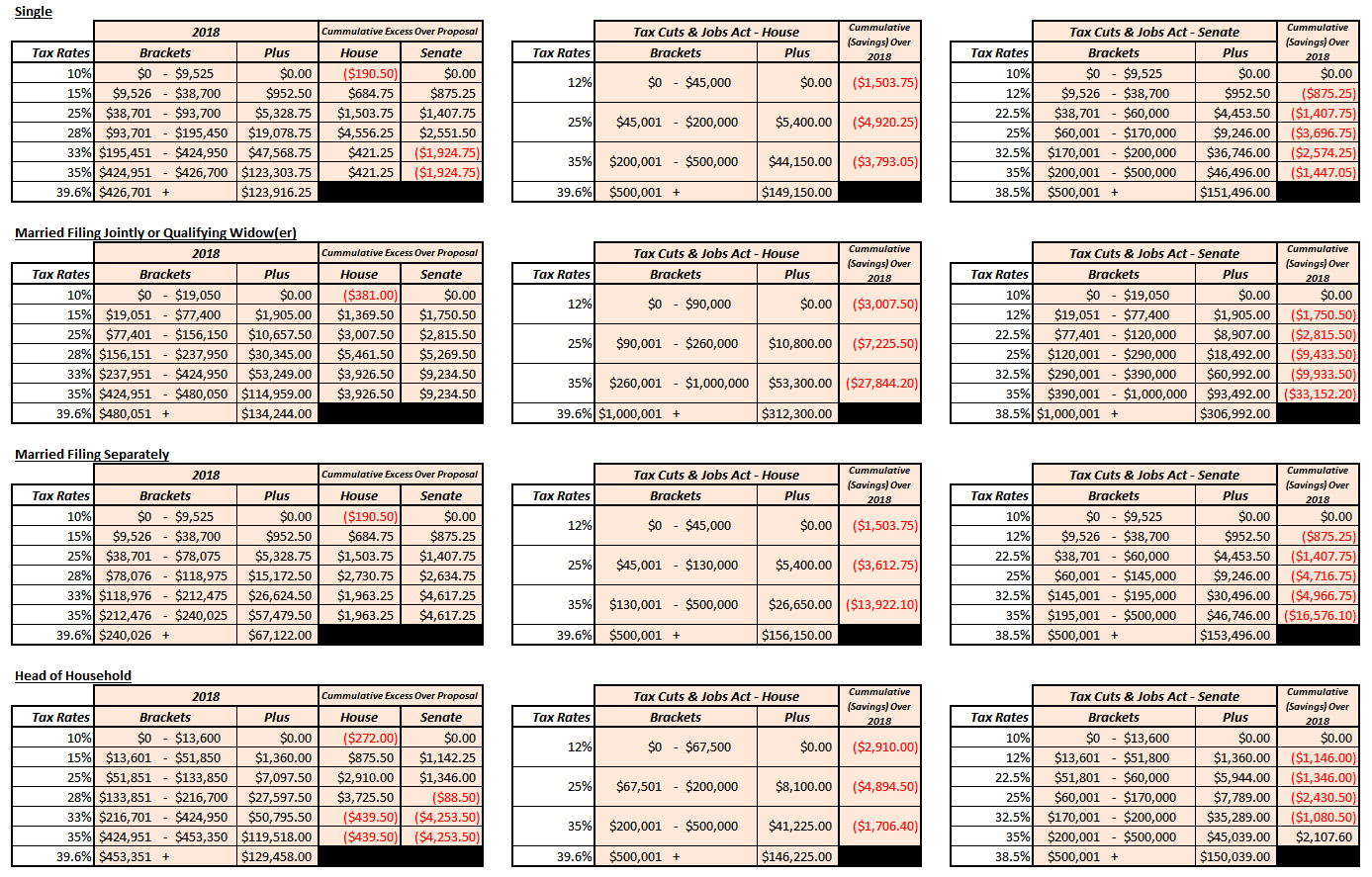

Tax Brackets

The House tax bill proposes to simplify the progressive tax structure by reducing the number of tax brackets from 7 to 4, which calls for a complete rethink of the stratification and width of each bracket. The Senate tax bill, on the other hand, proposes to retain 7 tax brackets but would realign the tax brackets with the introduction of 4 new rates. The tables below illustrate how the Senate and House proposals stack up against the 2018 tax rate schedules. As it stands at the moment, the 3.8% Net Investment Income Tax will continue to apply. Expatriates should also be mindful that their tax liabilities could still be affected by these changes, to the extent they have any taxable income, even if their compensation could be fully excluded by foreign earned income and housing exclusions as these exclusions must be taken into account for the determination of marginal tax rates.

Update: As of November 14, 2017, the Senate amendment would modify the thresholds for Head of Household filing status.

| Observations | House Tax Bill | Senate Tax Bill |

|---|---|---|

| Current 33% Tax Brackets | Taxpayers in these brackets under current structure will generally see smaller tax savings than those in the lower brackets because substantial portions of the 33% brackets will be incorporated into the proposed 35% brackets. This is especially marked for Single and Head of Household taxpayers due primarily to the reassignment of thresholds. | Married taxpayers in these brackets under the current structure will generally see larger tax savings than those in the lower brackets because substantial portions of the 33% brackets will be incorporated into the proposed 25% and 32.5% brackets.

Single and Head of Household taxpayers may, however, see an increase in tax because substantial portions of the 33% brackets will be incorporated into the proposed 35% brackets. |

| Proposed 35% Tax Brackets | Married taxpayers with high income within the proposed 35% brackets (up to $1,000,000 for MFJ and $500,000 for MFS) may stand to gain the most from these changes, without which, approximately 70% of the income within this proposed bracket would have been subject to tax at 39.6%. | Similarly, married taxpayers with high income within the proposed 35% brackets (up to $1,000,000 for MFJ and $500,000 for MFS) may stand to gain the most from these changes, without which, approximately 85% of the income within this proposed bracket would have been subject to tax at 39.6%. |

| Taxpayers in Proposed Top Brackets | Taxpayers whose adjusted gross income is in excess of $1 million ($1.2 million for MFJ) will not fully benefit from the 12% bracket. The tax benefit of the 12% bracket will be subject to phaseout at 6%. | High-income taxpayers subject to the proposed 38.5% bracket will stand to gain from the rate reduction from 39.6%. This could be especially beneficial to married taxpayers. |

Maximum Capital Gains Rate

There would be no material change to the existing capital gain tax regime for long-term capital gains and qualified dividends. Dollar thresholds of the tax brackets under current law, adjusted for inflation, would still be referenced for the determination of applicable capital gain tax rates in spite of the proposed realignments.

| Capital Gains Rate | 2018 | House Tax Bill | Senate Tax Bill |

|---|---|---|---|

| 20% | 39.6% tax bracket | 39.6% bracket under present law*: Single: $425,800 MFJ: $479,000 MFS: $239.500 HoH: $452,400 |

|

| 0% | 15% or lower tax brackets | At or below 15% bracket under present law*: MFJ: $77,200 Single/MFS: $38,600 HoH: $51,700 |

|

| 15% | Other tax brackets | Other than the ranges above* | |

| 25% (Max Rate) | Unrecaptured §1250 gain on depreciation | ||

| 28% (Max Rate) | Collectibles and §1202 Qualified Small Business Stock | ||

* Indexed for inflation. These figures differ from those published by the IRS in Rev. Proc. 2017-58.

Repeal of Alternative Minimum Tax

Both the House and Senate tax bills propose to repeal the Alternative Minimum Tax (AMT), a complex parallel tax system originally designed to ensure wealthy taxpayers who may otherwise exploit various deductions would pay a minimum amount of income tax but has since affected about 4.5 million families. However, the timing of when Minimum Tax Credit (MTC) carryover may be refunded differs slightly. Expatriates who had paid AMT on “deferral items,” such as Incentive Stock Options (ISO), which cause merely timing difference in income recognition, should continue to keep track of their AMT for the purpose of claiming Minimum Tax Credit (MTC).

| Refundable MTC | House Tax Bill | Senate Tax Bill |

|---|---|---|

| 50% of Excess | 2019 to 2021 | 2018 to 2020 |

| Full Refund | 2022 | 2021 |

Maximum Tax Rate on Business Income of Individuals

There are major differences between the House and Senate tax bills on the taxation of business income from small and family-owned businesses conducted as sole proprietorships, partnerships and S-corporations. The amended House tax bill has incorporated a provision to provide a new 9% tax rate, to be phased in over 5 years, for small businesses with net active business income, while retaining the 25% maximum rate, to garner the support of the National Federation of Independent Business, which is also reportedly supportive of the Senate’s version of the tax bill that provides for a 17.4% deduction.

Expatriates should note, nevertheless, that the concession proposed by the Senate refers specifically to “domestic qualified business income”, which is not defined in the Chairman’s Mark. It is possible that income from foreign pass-through entities may not be eligible under the Senate provision. Furthermore, expatriates who own or plan to start non-per se corporations with limited liability outside the U.S. should review how “check-the-box” election of foreign eligible entity may impact their overall tax liabilities in light of this and other provisions in the tax plan. Where capital is a material income producing factor of the trade or business, expatriates should also note that there would be no change to the allowance of up to 30% in net profits that may be deemed compensation for the purpose of foreign earned income exclusion.

| Taxation of Pass-Through Entities | House Tax Bill | Senate Tax Bill |

|---|---|---|

| Specific Service Businesses* | Not qualified | Not qualified but exception applies (see Income Limitations below) |

| Wages and Remuneration for Services Rendered | Not qualified | |

| Investment Income | Excluded | |

| Labor/Capital Percentage Presumption | Passive Business Activities: 100% Capital

Active Business Activities: 30% Capital+ 70% Labor, unless a binding 5-year election is made to apply a higher capital percentage as determined by a formula |

Not applicable |

| Tax Rates | Maximum Rate on Qualified Business Income: 25%

Reduced Rate on Net Active Business Income: |

Deduction of 17.4% from domestic qualified business income, essentially reducing maximum tax rate to about 32% |

| Income Limitations | Reduced Rate Applies Only to Qualified Active Business Income of Up To: MFJ: $75,000 MFS/Single: $37,500 HoH: $56,250 Reduced Rate Phaseout for Taxable Income Between:MFJ: $150,000 to $225,000 |

17.4% Deduction for Taxpayers with Domestic Qualified Business Income from Specific Services Businesses Phased Out for Taxable Income Between: MFJ: $100,000 to $150,000 Others: $50,000 to $75,000 |

| Anti-Avoidance Provision | Capital percentage would be limited if actual wages or income treated as received in exchange for services (e.g. a guaranteed payment) exceeds the taxpayer’s otherwise applicable capital percentage | Deduction limited to 50% of taxpayer’s W-2 if individual has qualified business income from partnership or S-corporation |

| Self-Employment Tax | No change to current law | |

* Any trade or business activity involving the performance of services in the fields of health, law, engineering, architecture, accounting, actuarial science, performing arts, consulting, athletics, financial services, brokerage services, or any trade or business where the principal asset of such trade or business is the reputation or skill of one or more of its employees.

Enhancement of Standard Deduction and Repeal of Personal Exemptions

Both the House and Senate tax bills propose to increase standard deduction and repeal personal exemptions in favor of a higher Child Tax Credit, albeit minute differences in terms of quantum. While the proposed increases may seem generous at first, it should be noted that these have already incorporated personal exemption(s) otherwise allowable under current law for the taxpayer (and spouse). Perhaps a more significant effect is that these increases, together with the proposed repeal of various deductions, would curtail taxpayers’ ability to itemize their deductions (and benefit from the deduction of personal exemptions at the same time under current law).

| Standard Deduction and Personal Exemption | 2018 | House Tax Bill | Senate Tax Bill | |

|---|---|---|---|---|

| Single | $6,500 | $12,200 | $12,000 | |

| Married Filing Jointly or Qualified Widow(er) | $13,000 | $24,400 | $24,000 | |

| Married Filing Separately | $6,500 | $12,200 | $12,000 | |

| Head of Household | $9,550 | $18,300 | $18,000 | |

| Additional Deduction (Per Person) |

Aged or Blind | $1,300 | Nil | $1,300 |

| And Unmarried But Not Surviving Spouse | $1,600 | Nil | $1,600 | |

| Exemption Amount | $4,150 | Nil | ||

Enhancement of Child Tax Credit and New Family Tax Credit

The House and Senate tax bills diverge on the availability of Family Tax Credit and thresholds for the phaseout of Child Tax Credit. The Senate tax bill proposes a slightly higher Child Tax Credit, but only by $50, increases the age limit of qualifying child by 1 year to 17, and generously raises the threshold for phaseout to $500,000 ($1 million for MFJ). On the other hand, the Family Tax Credit proposed by the House is absent in the Senate tax bill, which, instead, provides a $500 nonrefundable credit for qualifying dependents other than qualifying children. These would impact taxpayers differently, depending on the make-up of their household.

The increases in child tax credit and thresholds for phaseout are, indeed, welcome news as more expatriates should be able to benefit from the credit. Nevertheless, expatriates with qualifying dependents, for whom personal exemptions would have been allowed under existing law, may find themselves losing the benefits of these exemptions as the credits proposed by both tax bills might not quite make up for the loss, even at the top marginal rates.

| Child Tax Credit and Family Tax Credit | 2018 | House Tax Bill | Senate Tax Bill | |

|---|---|---|---|---|

| Child Tax Credit | Amount | $1,000 | $1,600 | $1,650 |

| Age Limit | 16 | 16 | 17 | |

| Taxpayer | Nil | $300 | Nil | |

| Spouse | Nil | $300 | Nil | |

| Non-Child Dependent | Nil | $300 | $500 | |

| MAGI Phaseout Threshold | Single | $75,000 | $115,000 | $500,000 |

| Married Filing Jointly or Qualified Widow(er) | $110,000 | $230,000 | $1 million | |

| Married Filing Separately | $55,000 | $115,000 | $500,000 | |

| Head of Household | $75,000 | $115,000 | $500,000 | |

Simplification and Reform of Deductions

Many of the familiar deductions would be repealed, although there are some differences between the House’s and Senate’s tax bills. It is anticipated that these changes would result in fewer than 10% of the taxpayers choosing to itemize their deductions, compared to about 33% today. The proposed repeal of state and local income taxes is one of the most contentious topic for states with high taxes; it remains to be seen whether some level of deduction would be reinstated if the tax bill is to be enacted.

Expatriates who have not broken tax residency with states, due to domiciliary or other reasons, particularly those that do not allow foreign earned income exclusion and/or foreign tax credit may like to reconsider their state tax residency in light of the proposed changes. Our observations of how the changes proposed by the House tax bill could affect expatriates and what they should considered can be found in our previous newsletter.

| House Tax Bill | Senate Tax Bill | |||

| Above-the-Line Deductions | Alimony Payments | Repealed | No change to current law | |

| Moving Expenses | Repealed (Only deductible for military members) | |||

| Medical Savings Account | Repealed | No change to current law | ||

| Student Loan Interest | Repealed | No change to current law | ||

| Tuition and Fees | Repealed | No change to current law | ||

| Itemized Deductions | Medical Expenses | Repealed | No change to current law | |

| Mortgage Interest | Principal Residence | Limited to $500,000 ($250,000 for MFS) for loans after November 2, 2017* | No change to current law | |

| Vacation Home | Repealed | |||

| Refinancing | No change to current law, subject to relevant limits. | |||

| Home Equity Loan | Repealed | |||

| State and Local Income Taxes or Sales Taxes | Repealed | |||

| Foreign Income Tax | No change to current law | |||

| State, Local, and Foreign Property Tax | State and local real property taxes only. Limited to $10,000 ($5,000 for MFS) | Repealed | ||

| Tax Preparation Expenses | Repealed | |||

| Employee Business Expenses | Repealed | |||

| Personal Casualty Losses | Repealed (unless associated with special disaster relief legislation) | |||

* The related indebtedness would be deductible under current law if (i) a written binding contract was entered into prior to November 2, 2017 for closing the purchase of a principal residence before January 1, 2018 and (ii) the purchase of such residence does take place before April 1, 2018.

Simplification and Reform of Exclusions and Taxable Compensation

The House and Senate take a similar stance on the exclusion of gain from the sale of principal residence. With the repeal of exclusion for employer-provided housing generating less than $50 million of additional revenue as estimated by JCT, this provision does not appear to be a priority for the Senate Finance Committee and is not included in the Senate tax bill.

| Exclusions | 2018 | House Tax Bill | Senate Tax Bill | |

|---|---|---|---|---|

| Employer-Provided Housing | Fully excludable | Limited to $50,000 ($25,000 for MFS), subject to phaseout for “highly compensated employees”* | No change to current law | |

| Gain from Sale of Principal Residence | Ownership and Use Requirements | 2 out of 5 years | 5 out of 8 years | |

| Failure to Meet Certain Requirements^ | Prorated over 2 years | Prorated over 5 years | ||

| Limitations | $250,000 ($500,000 for MFJ) | Limit reduced, but not below zero, by excess of (a) average modified adjusted gross income for 3 year over (b) $250,000 ($500,000 for MFJ) | No change to current law | |

| Frequency of Exclusion | Once every 2 years | Once every 5 years | ||

* With compensation in excess of $120,000 for 2018, as adjusted for inflation.

^ By reason of a change of place of employment, health, or, to the extent provided under regulations, unforeseen circumstances.

The House tax bill does not contain language about how the proposed changes to employer-provided housing, to the extent not fully excluded, would coordinate with the operation of foreign housing exclusion as the provision appears to be domestically-focused. Expatriates living in employer-provided camp housing, which is a common arrangement in countries such as Saudi Arabia, should continue to monitor the development. Even if the cost of camp housing becomes eligible for foreign housing exclusion, expatriates, whose compensation exceeds the limitation for foreign earned income exclusion, may incur a higher tax liability than under current law because the base housing amount ($16,656 for 2018) is not excludable and as a result of the stacking rule, which may put them in a higher tax bracket.

Expatriates who have not used their homes in the U.S. for some years due to their assignment/employment overseas and were relying on the 2 out of 5 year rule under current law to maximize their excludable gain may now need to reconsider their plan in the event this provision is enacted. High-income expatriates with impending transactions in which substantial income would be recognized (e.g. stock option exercise, bonus payment, sell of stocks, etc.) should also consider the timing of such transactions relative to the closing of their home sale.

Estate, Gift, and Generation-Skipping Transfer Taxes

The Senate tax bill, unlike the House’s, does not include either the repeal of estate tax and generation-skipping transfer taxes or a rate reduction for gift tax. Both tax bill, however, would double the estate tax basic exclusion amount from 2018. Expatriates who are not U.S. citizens and those with non-U.S. spouses will see no additional reprieve.

| House Tax Bill | Senate Tax Bill | |

|---|---|---|

| Estate Tax | Repealed from 2024 | No change to current law |

| Generation-Skipping Transfer Tax | ||

| Basic Exclusion Amount | Doubled to $10 million (as of 2011 value), indexed for inflation | |

| Gift Tax | Top rate lowered to 35% from 2024 | No change to current law |

Retirement Savings Provision Included Only in the Senate Tax Bill

As of November 14, 2017, the Senate amendment would:

- Require all catch up contributions to section 401(k), 403(b), and 457(b) retirement savings plans to be Roth only; and

- Increase the $6,000 catch-up contribution annual limit applicable to such plans to $9,000

This is more favorable than the original proposal, which would disallow employees, who are aged 50 or over, from making catch-up contributions for a year if the individual received wages of $500,000 or more for the preceding year. While contributions to Roth IRA is not tax deductible, no tax would be due on the earnings and qualified distributions. Given the proposed amendment, it seems likely that special provisions would be made for high-income taxpayers, who would otherwise be ineligible for Roth IRA contributions under current law (see previous newsletter), to make the relevant catch-up contributions.

Other Provisions Included Only in the House Tax Bill

(A) Simplification and Reform of Education Incentives:

The Lifetime Learning Credit (LLC) will be consolidated into an enhanced American Opportunity Tax Credit (AOTC). Unlike LLC under current law, however, the enhanced AOTC may only be claimed for the first 5 years of post-secondary education at an eligible educational institution and the credit for the fifth year would only be at half the rate (as the first four years), with up to $500 of such credit being refundable.

(B) Consolidation of Education Savings Rules:

No new contributions to Coverdell education savings accounts would be allowed after 2017 (except rollover contributions) but tax-free rollovers from Coverdell accounts into section 529 plans would be allowed. On the other hand, elementary and high school expenses of up to $10,000 per year would be considered qualified expenses for section 529 plans. Qualified expenses would also be expanded to cover expenses associated with apprenticeship programs.

In addition, rollovers from section 529 plans to Achieving a Better Life Experience (ABLE) section 529A accounts would be allowed.

(C) Repeal of Other Provisions Related to Education:

The following exclusions related to education would be repealed –

- U.S. savings bond interest exclusion

- Exclusion for qualified tuition reduction programs

- Exclusion for employer-provided education assistance programs

American Expatriate Tax is a part of Contexo Global Mobility Solutions & Tax Consulting Ltd. registered in Hong Kong. Together, we help companies and individuals navigate through the complexities of global mobility and related tax issues. Here is where you will find a blend of expertise from Big 4 accounting firms and Fortune Global 500 companies but the attention of a boutique consulting practice. The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.